Monday, June 8, 2009

TSCC Update

The Technology Solutions Company liquidation arbitrage has been remarkably successful. On May 1st the Company made its initial liquidating distribution for $2.15/share in cash, an amount that was much higher than the Company's original $2/share estimate. Moreover, the Company has already appointed a trustee and expects to collect its remaining net assets receivables over the next couple of months. When that process is completed the Company should make an additional liquidating distribution of about $0.33/share (hence the current share price), an amount that would place the total liquidation proceeds around $2.48/share, which is consistent with the Company's original liquidation estimate of $2.47/share. When I originally wrote about the TSCC liquidation arbitrage in mid-March the stock traded for $2.12/share. The initial liquidating distribution has already made the trade profitable by $0.02/share, thereby removing all the downside risk (just as predicted) Moreover, the remaining $0.33/share distribution will bring the total dollar profit to $0.36/share, thereby yielding16.98% in less than 5 months, or 40.75% on an annualized basis and with virtually no risk.

Monday, April 13, 2009

Entrust, Inc. Thomas Bravo Merger

Today, Thomas Bravo, Inc, a private equity firm based out of Chicago, offered to acquire Entrust Inc. for $1.85/share in cash. Pursuant to the merger agreement, Entrust is allowed to solicit potential suitors over the next 30 days. In my opinion, the cash consideration is very low, a situation which could potentially cause a bidding war between interested parties (if there are any). Nonetheless, Thomas Bravo has demonstrated is capacity to pay through a combination of equity and debt commitments. I suspect the equity commitment will be internally funded by Thomas Bravo (the company recently raised approximately $800M). Thomas Bravo, should also have relatively little problems integrating the business given that the company specializes in acquiring technology based companies. Therefore, should the deal be approved, the close should go rather smoothly (absent shareholder litigation). A long/short hedge fund based out of Connecticut, however, owns a large stake in Entrust, which may complicate approval of the merger. The transaction should close relatively quickly given that it is an all cash deal (i.e. no registration statement must be filed for the issuance of securities). Moreover, shareholder approval is only required by Entrust. Consequently, the transaction should close in about 1-2 months. Downside risk is around $0.20 (stock traded around $1.60 pre-announcement). The stock currently trades for $1.80. Therefore, assuming an 85%-90% chance of success, the RAAR is approximately 4.22%-8.45%, which represents a significant premium to 3-month T-Bills. I will await the filing of Form 8-K and the Definitive Proxy.

Image Update

We're well through early trading today and Image has not released any information related to the Nyx deposit. I suspect that Nyx has failed to make the payment and that the parties have entered into another round of negotiations. However, the stock is holding up well given the lack of news (essentially unchanged; currently trading at $1.40). I find the lack of price movement somewhat unusual. Maybe someone has some information related to the transaction (historically, there has been quite a few leaks with the Image transaction). If this is the case, the buoyed stock price may be indicative of the fact that Nyx and Image are finalizing the transaction. However, given that Image has not released any press release, this explanation is probably unlikely.

Wednesday, April 8, 2009

Image Entertainment Merger - Analysis & Update

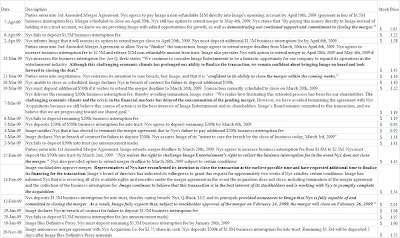

The Image/Q-Black transaction has been an eventful one to say the least (refer to calendar below). The deal, which was negoitated on Nov. 20th, 2008, has already been through 3 amended merger agreenents, 1-2.5M in non-refundable fees and deposits, and an extension to April 20th, 2009 to close the merger.

In the most recent upset, Nyx Acquistion Co. has failed (yet again) to make a timely payment of an agreed upon increase in the business interruption fee. The payment disruption is yet another example of how Nyx has struggled to "finalize" financing with Q-Black, the elusive financier who provided the original equity committment letter back in Novemeber. Unfortunately, that equity "committment" seems to have dissappeared in the face of a "challenging economic climate and crisis in the financial markets." Oddly, the parties have remained relatively silent about the specifics of that statement, a situation which has left many investors questioning whether financing has been entirely wiped out or simply imparied. The recurrent payment disruptions would certainly suggest that it is the former, a fact that has seriously questioned the likelihood of the transaction closing. With Image now trading at $1.45/share, the Street is essentially pricing in an 80-85% chance of failure.

However, despite the recurrent payment hiccupps, Nyx and Image remain oddly committed to closing the transaction. On April 7th, 2009, for example, Nyx stated that it was in "continued support and committment to closing the merger." The statement was made in coordination with its failure to deposit a $1.5M business interruption fee. On March, 24th, 2009 Nyx made a similar statement when it indicated that "Although, this challenging economic climate has prolonged our ability to finalize the transaction we remain confident about bringing Image on-board and look forward to closing the deal." The statements, which are apart of string of similar statements made on March 7th, March 2nd, and February 12th, suggest that Nyx and Image are partially optimistic about the close, at least greater than the implied probabilities of 15-20%. In fact, Nyx's statements would seem to suggest that the financing troubles are only ephemeral, and its constant agreements to increase the business interruption fee would too. After all, Nyx has already agreed to increase the business interruption fee from $1.8M to $2.5M, and could stand to lose as much as $3.5M (assuming the $1M non-refundable deposit is made on April 10th) should the transaction fail. This amount represents nearly 5% of the $79M transaction value and over 10% of Image's current market capitalizatoin. This fact, of course, raises some interesting questions. For one, if Nyx truly believed financing was in jeopardy why Nyx would it continue to throw money at Image? Would'nt Nyx have simply abandoned the merger back in February or March? Maybe, Nyx knows something about financing, a fact that has kept it committed to the transaction. Or, maybe, Nyx just really wants Image (after all its not paying much. Plus I'm sure Image is more than happy to collect the hefty business interruption fees that Nyx continues to pay).

Nonetheless, the ultimate questions is still whether or not Nyx will come up with the money? If history is any precusor to the future, it probably won't (although, there is a good chance that it will cure shortly thereafter). Either way, Image remains an attractive acquisition target. Moreover, the return characteristics of the transaction are enormosly appealing. After all, Image currently trades for $1.45; Nyx has agreed to pay $2.75/share in cash; and, given that the S&P500 has increased about 20% since mid-March, the new downside low for Image is probably between $1.20-$1.30/share. Consequently, the risk/reward profile on this transction is compelling to say the least (about 4:1). If Nyx fails to make payment (which it probably will) the resulting downward move in Image's stock could provide an interesting entry point for those willing to bear the risk. Unfortunately, however, that risk could be pretty high.

{kind=link}

In the most recent upset, Nyx Acquistion Co. has failed (yet again) to make a timely payment of an agreed upon increase in the business interruption fee. The payment disruption is yet another example of how Nyx has struggled to "finalize" financing with Q-Black, the elusive financier who provided the original equity committment letter back in Novemeber. Unfortunately, that equity "committment" seems to have dissappeared in the face of a "challenging economic climate and crisis in the financial markets." Oddly, the parties have remained relatively silent about the specifics of that statement, a situation which has left many investors questioning whether financing has been entirely wiped out or simply imparied. The recurrent payment disruptions would certainly suggest that it is the former, a fact that has seriously questioned the likelihood of the transaction closing. With Image now trading at $1.45/share, the Street is essentially pricing in an 80-85% chance of failure.

However, despite the recurrent payment hiccupps, Nyx and Image remain oddly committed to closing the transaction. On April 7th, 2009, for example, Nyx stated that it was in "continued support and committment to closing the merger." The statement was made in coordination with its failure to deposit a $1.5M business interruption fee. On March, 24th, 2009 Nyx made a similar statement when it indicated that "Although, this challenging economic climate has prolonged our ability to finalize the transaction we remain confident about bringing Image on-board and look forward to closing the deal." The statements, which are apart of string of similar statements made on March 7th, March 2nd, and February 12th, suggest that Nyx and Image are partially optimistic about the close, at least greater than the implied probabilities of 15-20%. In fact, Nyx's statements would seem to suggest that the financing troubles are only ephemeral, and its constant agreements to increase the business interruption fee would too. After all, Nyx has already agreed to increase the business interruption fee from $1.8M to $2.5M, and could stand to lose as much as $3.5M (assuming the $1M non-refundable deposit is made on April 10th) should the transaction fail. This amount represents nearly 5% of the $79M transaction value and over 10% of Image's current market capitalizatoin. This fact, of course, raises some interesting questions. For one, if Nyx truly believed financing was in jeopardy why Nyx would it continue to throw money at Image? Would'nt Nyx have simply abandoned the merger back in February or March? Maybe, Nyx knows something about financing, a fact that has kept it committed to the transaction. Or, maybe, Nyx just really wants Image (after all its not paying much. Plus I'm sure Image is more than happy to collect the hefty business interruption fees that Nyx continues to pay).

Nonetheless, the ultimate questions is still whether or not Nyx will come up with the money? If history is any precusor to the future, it probably won't (although, there is a good chance that it will cure shortly thereafter). Either way, Image remains an attractive acquisition target. Moreover, the return characteristics of the transaction are enormosly appealing. After all, Image currently trades for $1.45; Nyx has agreed to pay $2.75/share in cash; and, given that the S&P500 has increased about 20% since mid-March, the new downside low for Image is probably between $1.20-$1.30/share. Consequently, the risk/reward profile on this transction is compelling to say the least (about 4:1). If Nyx fails to make payment (which it probably will) the resulting downward move in Image's stock could provide an interesting entry point for those willing to bear the risk. Unfortunately, however, that risk could be pretty high.

Emageon/AMICAS Update

On April 2nd, approximately 88% of Emageon's total outstanding stock was tendered, thereby closing the Emageon/AMICAS transaction. As expected, AMICAS executed its "top-up" option provision and completed the transaction as a short-form merger. The cash consideration of $1.82 per share was deposited into my account on April 3rd, yielding an annualized return of 27.87% againt my initial purchase price of $1.77/share on February 25th, 2009. Excellent transaction!

Friday, March 20, 2009

Technology Solutions - Update

On March 20th Hedonic Capital, LLC and TowerView, LLC reported initial acquistions of the Company's stock of 8.7% and 5.1%, respectively. Hedonic Capital, LLC appears to be a small hedge fund based out of Conneticut. The fund is managed by David Lu, who also runs another fund entitled Hedgehog, LLC. TowerView, LLC appears to be an investment house based in New York. My assumption is that both funds are relatively small (perhaps single man investment houses) since I was unable to find any significant information related to either of them. Nonetheless, I view both acquistions as positive given that they were most likely mode shortly after the filing of the preliminary proxy materials.

Image Enteratinment - Update

In the most recent upset with the Image/Q-Black deal, Nyx has failed to deliver the promised $500k deposit under the amended merger agreement. The failure of Nyx to deposit the money has caused a material breach and is yet another reflection of Nyx's inability to obtain the necessary financing to consumate the merger. While the Board of Image Entertainment plans to issue a press release after the close of business today indicating its intended action related to Nyx's breach, such action has failed to materialize. The failure of Image's Board to issue a press release is reminiscient of the Company's reporting (or lack thereof)that has characterized the entire merger process.

Subscribe to:

Comments (Atom)