Monday, June 8, 2009

TSCC Update

The Technology Solutions Company liquidation arbitrage has been remarkably successful. On May 1st the Company made its initial liquidating distribution for $2.15/share in cash, an amount that was much higher than the Company's original $2/share estimate. Moreover, the Company has already appointed a trustee and expects to collect its remaining net assets receivables over the next couple of months. When that process is completed the Company should make an additional liquidating distribution of about $0.33/share (hence the current share price), an amount that would place the total liquidation proceeds around $2.48/share, which is consistent with the Company's original liquidation estimate of $2.47/share. When I originally wrote about the TSCC liquidation arbitrage in mid-March the stock traded for $2.12/share. The initial liquidating distribution has already made the trade profitable by $0.02/share, thereby removing all the downside risk (just as predicted) Moreover, the remaining $0.33/share distribution will bring the total dollar profit to $0.36/share, thereby yielding16.98% in less than 5 months, or 40.75% on an annualized basis and with virtually no risk.

Monday, April 13, 2009

Entrust, Inc. Thomas Bravo Merger

Today, Thomas Bravo, Inc, a private equity firm based out of Chicago, offered to acquire Entrust Inc. for $1.85/share in cash. Pursuant to the merger agreement, Entrust is allowed to solicit potential suitors over the next 30 days. In my opinion, the cash consideration is very low, a situation which could potentially cause a bidding war between interested parties (if there are any). Nonetheless, Thomas Bravo has demonstrated is capacity to pay through a combination of equity and debt commitments. I suspect the equity commitment will be internally funded by Thomas Bravo (the company recently raised approximately $800M). Thomas Bravo, should also have relatively little problems integrating the business given that the company specializes in acquiring technology based companies. Therefore, should the deal be approved, the close should go rather smoothly (absent shareholder litigation). A long/short hedge fund based out of Connecticut, however, owns a large stake in Entrust, which may complicate approval of the merger. The transaction should close relatively quickly given that it is an all cash deal (i.e. no registration statement must be filed for the issuance of securities). Moreover, shareholder approval is only required by Entrust. Consequently, the transaction should close in about 1-2 months. Downside risk is around $0.20 (stock traded around $1.60 pre-announcement). The stock currently trades for $1.80. Therefore, assuming an 85%-90% chance of success, the RAAR is approximately 4.22%-8.45%, which represents a significant premium to 3-month T-Bills. I will await the filing of Form 8-K and the Definitive Proxy.

Image Update

We're well through early trading today and Image has not released any information related to the Nyx deposit. I suspect that Nyx has failed to make the payment and that the parties have entered into another round of negotiations. However, the stock is holding up well given the lack of news (essentially unchanged; currently trading at $1.40). I find the lack of price movement somewhat unusual. Maybe someone has some information related to the transaction (historically, there has been quite a few leaks with the Image transaction). If this is the case, the buoyed stock price may be indicative of the fact that Nyx and Image are finalizing the transaction. However, given that Image has not released any press release, this explanation is probably unlikely.

Wednesday, April 8, 2009

Image Entertainment Merger - Analysis & Update

The Image/Q-Black transaction has been an eventful one to say the least (refer to calendar below). The deal, which was negoitated on Nov. 20th, 2008, has already been through 3 amended merger agreenents, 1-2.5M in non-refundable fees and deposits, and an extension to April 20th, 2009 to close the merger.

In the most recent upset, Nyx Acquistion Co. has failed (yet again) to make a timely payment of an agreed upon increase in the business interruption fee. The payment disruption is yet another example of how Nyx has struggled to "finalize" financing with Q-Black, the elusive financier who provided the original equity committment letter back in Novemeber. Unfortunately, that equity "committment" seems to have dissappeared in the face of a "challenging economic climate and crisis in the financial markets." Oddly, the parties have remained relatively silent about the specifics of that statement, a situation which has left many investors questioning whether financing has been entirely wiped out or simply imparied. The recurrent payment disruptions would certainly suggest that it is the former, a fact that has seriously questioned the likelihood of the transaction closing. With Image now trading at $1.45/share, the Street is essentially pricing in an 80-85% chance of failure.

However, despite the recurrent payment hiccupps, Nyx and Image remain oddly committed to closing the transaction. On April 7th, 2009, for example, Nyx stated that it was in "continued support and committment to closing the merger." The statement was made in coordination with its failure to deposit a $1.5M business interruption fee. On March, 24th, 2009 Nyx made a similar statement when it indicated that "Although, this challenging economic climate has prolonged our ability to finalize the transaction we remain confident about bringing Image on-board and look forward to closing the deal." The statements, which are apart of string of similar statements made on March 7th, March 2nd, and February 12th, suggest that Nyx and Image are partially optimistic about the close, at least greater than the implied probabilities of 15-20%. In fact, Nyx's statements would seem to suggest that the financing troubles are only ephemeral, and its constant agreements to increase the business interruption fee would too. After all, Nyx has already agreed to increase the business interruption fee from $1.8M to $2.5M, and could stand to lose as much as $3.5M (assuming the $1M non-refundable deposit is made on April 10th) should the transaction fail. This amount represents nearly 5% of the $79M transaction value and over 10% of Image's current market capitalizatoin. This fact, of course, raises some interesting questions. For one, if Nyx truly believed financing was in jeopardy why Nyx would it continue to throw money at Image? Would'nt Nyx have simply abandoned the merger back in February or March? Maybe, Nyx knows something about financing, a fact that has kept it committed to the transaction. Or, maybe, Nyx just really wants Image (after all its not paying much. Plus I'm sure Image is more than happy to collect the hefty business interruption fees that Nyx continues to pay).

Nonetheless, the ultimate questions is still whether or not Nyx will come up with the money? If history is any precusor to the future, it probably won't (although, there is a good chance that it will cure shortly thereafter). Either way, Image remains an attractive acquisition target. Moreover, the return characteristics of the transaction are enormosly appealing. After all, Image currently trades for $1.45; Nyx has agreed to pay $2.75/share in cash; and, given that the S&P500 has increased about 20% since mid-March, the new downside low for Image is probably between $1.20-$1.30/share. Consequently, the risk/reward profile on this transction is compelling to say the least (about 4:1). If Nyx fails to make payment (which it probably will) the resulting downward move in Image's stock could provide an interesting entry point for those willing to bear the risk. Unfortunately, however, that risk could be pretty high.

{kind=link}

In the most recent upset, Nyx Acquistion Co. has failed (yet again) to make a timely payment of an agreed upon increase in the business interruption fee. The payment disruption is yet another example of how Nyx has struggled to "finalize" financing with Q-Black, the elusive financier who provided the original equity committment letter back in Novemeber. Unfortunately, that equity "committment" seems to have dissappeared in the face of a "challenging economic climate and crisis in the financial markets." Oddly, the parties have remained relatively silent about the specifics of that statement, a situation which has left many investors questioning whether financing has been entirely wiped out or simply imparied. The recurrent payment disruptions would certainly suggest that it is the former, a fact that has seriously questioned the likelihood of the transaction closing. With Image now trading at $1.45/share, the Street is essentially pricing in an 80-85% chance of failure.

However, despite the recurrent payment hiccupps, Nyx and Image remain oddly committed to closing the transaction. On April 7th, 2009, for example, Nyx stated that it was in "continued support and committment to closing the merger." The statement was made in coordination with its failure to deposit a $1.5M business interruption fee. On March, 24th, 2009 Nyx made a similar statement when it indicated that "Although, this challenging economic climate has prolonged our ability to finalize the transaction we remain confident about bringing Image on-board and look forward to closing the deal." The statements, which are apart of string of similar statements made on March 7th, March 2nd, and February 12th, suggest that Nyx and Image are partially optimistic about the close, at least greater than the implied probabilities of 15-20%. In fact, Nyx's statements would seem to suggest that the financing troubles are only ephemeral, and its constant agreements to increase the business interruption fee would too. After all, Nyx has already agreed to increase the business interruption fee from $1.8M to $2.5M, and could stand to lose as much as $3.5M (assuming the $1M non-refundable deposit is made on April 10th) should the transaction fail. This amount represents nearly 5% of the $79M transaction value and over 10% of Image's current market capitalizatoin. This fact, of course, raises some interesting questions. For one, if Nyx truly believed financing was in jeopardy why Nyx would it continue to throw money at Image? Would'nt Nyx have simply abandoned the merger back in February or March? Maybe, Nyx knows something about financing, a fact that has kept it committed to the transaction. Or, maybe, Nyx just really wants Image (after all its not paying much. Plus I'm sure Image is more than happy to collect the hefty business interruption fees that Nyx continues to pay).

Nonetheless, the ultimate questions is still whether or not Nyx will come up with the money? If history is any precusor to the future, it probably won't (although, there is a good chance that it will cure shortly thereafter). Either way, Image remains an attractive acquisition target. Moreover, the return characteristics of the transaction are enormosly appealing. After all, Image currently trades for $1.45; Nyx has agreed to pay $2.75/share in cash; and, given that the S&P500 has increased about 20% since mid-March, the new downside low for Image is probably between $1.20-$1.30/share. Consequently, the risk/reward profile on this transction is compelling to say the least (about 4:1). If Nyx fails to make payment (which it probably will) the resulting downward move in Image's stock could provide an interesting entry point for those willing to bear the risk. Unfortunately, however, that risk could be pretty high.

Emageon/AMICAS Update

On April 2nd, approximately 88% of Emageon's total outstanding stock was tendered, thereby closing the Emageon/AMICAS transaction. As expected, AMICAS executed its "top-up" option provision and completed the transaction as a short-form merger. The cash consideration of $1.82 per share was deposited into my account on April 3rd, yielding an annualized return of 27.87% againt my initial purchase price of $1.77/share on February 25th, 2009. Excellent transaction!

Friday, March 20, 2009

Technology Solutions - Update

On March 20th Hedonic Capital, LLC and TowerView, LLC reported initial acquistions of the Company's stock of 8.7% and 5.1%, respectively. Hedonic Capital, LLC appears to be a small hedge fund based out of Conneticut. The fund is managed by David Lu, who also runs another fund entitled Hedgehog, LLC. TowerView, LLC appears to be an investment house based in New York. My assumption is that both funds are relatively small (perhaps single man investment houses) since I was unable to find any significant information related to either of them. Nonetheless, I view both acquistions as positive given that they were most likely mode shortly after the filing of the preliminary proxy materials.

Image Enteratinment - Update

In the most recent upset with the Image/Q-Black deal, Nyx has failed to deliver the promised $500k deposit under the amended merger agreement. The failure of Nyx to deposit the money has caused a material breach and is yet another reflection of Nyx's inability to obtain the necessary financing to consumate the merger. While the Board of Image Entertainment plans to issue a press release after the close of business today indicating its intended action related to Nyx's breach, such action has failed to materialize. The failure of Image's Board to issue a press release is reminiscient of the Company's reporting (or lack thereof)that has characterized the entire merger process.

Monday, March 16, 2009

Emageon Merger Arbitrage - Update

On March 11th, 2009 a putative class action law suit was filed againat Emageon and AMICAS claiming that the Company breached its fudiciary duty when negotiating the merger. The plaintiffs seeks to enjoin the trasnaction. Both Emageon and AMICAS (and myself) believe the lawsuit is without merit. Nonetheless, the currently pending lawsuit could lengthen the time until closing.

Technology Solutions Liquidation - Update

Today, Technology Solutions Company (TICKER: TSCC) filed its preliminary proxy materials related to the Plan of Complete Liquidation and Dissolution of the Company. According to the plan (and consistent with my prior post and original Plan), the Company expects to make an initial liquidating distribution of at least $2/share immediately following shareholder approval of the Plan. In addition, the Company stated that the initial liquidating distribution could be higher, depending on when the non-cash assets are monetized. Also, as indicated in the Plan the Company intends to make additional liquidating distributions to the shareholders. Total distributions are expected to range from $2.39 to $2.69 per share in cash, which is inclusive of the initial liquidating distribution of $2/share. The stock closed up to $2.30 today, or 8.49% above the $2.12 price mentioned in my original post last week.

The company anticipates that a majority of the remaining distributions will be made by the end of 2009.

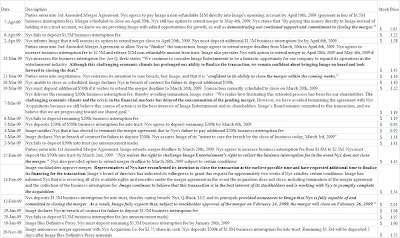

Summary of Liquidation Estimets (Preliminary Proxy pg. 23)

The table above demonstrates that a considerable portion of the expected liquidation distributions will come from assets with highly ascertainable values. Over 78.8% of the total estimated assets (based upon the low estimate) is cash deposited at the Harris Bank in Chicago. The expected cash collections are primarily trade receivables due from various hospitals, which should be collected with virtually little problems.

The primary note collections are related entirely to two outstanding notes from the sale of the Company's subsidiary companies. The first note is payable by EnteGreat Solutions, LLC for the sale of the Company's SAP Practice. The total amount due under the note is $380,271, and is due April 29, 2009. The second note is payable by Valkre Solutions, Inc. for the sale of the Company's CVC Practice, and is due in two equal installments on March, 31st and June 30th 2009 for $135,918 (I suspect that these values, when added together, are slightly higher than the value indicated in the table because the Company discounted them). Moreover, the interest earned relates to interest payable on the cash balances on the Company's bank account. Collectively, these assets equal over 95.66% of the estimated realizable value of the Company's assets under the low estimate; these value should not change going forward, and if they do their effect on the ultimate distribution will be de minimis.

While the prelimary proxy materials do not provide detailed infomation on the assets underlying the "estimated sale of assets" category of their liquidation distribution estimates, the amount is most likely related to approximately $768,000 in capitalized software and development costs for the Company's Blue Ocean medical software, which reached technological feasibility during the 2nd quarter of FY 2008. I suspect that these assets will be sold relatively quickly due to a one line sentence in the Background portion of the preliminary proxy materials that states: "Since the announcement of the approval of the Plan of Dissolution by the Board, Mr. Silva-Craig has been approached by numerous parties with respect to the possible purchase of various assets of the Company." Also, as aside another party who is interested in effecting a reverse merger with the Company has contacted Mr. Silvia, a transaction which, if structured correctly, could lead to additional value for TSCC shareholders.

The only real uncertainty is related to the total estimated liabilities. I must admit that estimating the total amount of such expenses is totally beyond my level of competence. However, I believe a reasonable margin of safety is to increase the high estimate by 10-15%. Under such an assumption total estimated liabilities would range between $2,756,122.6 and $2,881,400.9. Thus, if the non-cash assets are sold for the average of the low and high estimate, or approximately $687,500, then the "likely" distribution could range between $2.36-$2.41/share, which is near the Company's low estimate. The 10-15% increase in high expenses, however, may be entirely unreasonable given that most of the estimated expenses are fixed. Therefore, if we simply use the Company's high estimate as a proxy for total expenses, then the "likely" estimated distribution is approximately $2.51/share, which represents a decent premium to my acquistion price of $2.12/share (approximately 18.39%, or 24.52% on an annualized basis if we assume distriubtions are made on or before December 31st, 2009).

The company anticipates that a majority of the remaining distributions will be made by the end of 2009.

Summary of Liquidation Estimets (Preliminary Proxy pg. 23)

The table above demonstrates that a considerable portion of the expected liquidation distributions will come from assets with highly ascertainable values. Over 78.8% of the total estimated assets (based upon the low estimate) is cash deposited at the Harris Bank in Chicago. The expected cash collections are primarily trade receivables due from various hospitals, which should be collected with virtually little problems.

The primary note collections are related entirely to two outstanding notes from the sale of the Company's subsidiary companies. The first note is payable by EnteGreat Solutions, LLC for the sale of the Company's SAP Practice. The total amount due under the note is $380,271, and is due April 29, 2009. The second note is payable by Valkre Solutions, Inc. for the sale of the Company's CVC Practice, and is due in two equal installments on March, 31st and June 30th 2009 for $135,918 (I suspect that these values, when added together, are slightly higher than the value indicated in the table because the Company discounted them). Moreover, the interest earned relates to interest payable on the cash balances on the Company's bank account. Collectively, these assets equal over 95.66% of the estimated realizable value of the Company's assets under the low estimate; these value should not change going forward, and if they do their effect on the ultimate distribution will be de minimis.

While the prelimary proxy materials do not provide detailed infomation on the assets underlying the "estimated sale of assets" category of their liquidation distribution estimates, the amount is most likely related to approximately $768,000 in capitalized software and development costs for the Company's Blue Ocean medical software, which reached technological feasibility during the 2nd quarter of FY 2008. I suspect that these assets will be sold relatively quickly due to a one line sentence in the Background portion of the preliminary proxy materials that states: "Since the announcement of the approval of the Plan of Dissolution by the Board, Mr. Silva-Craig has been approached by numerous parties with respect to the possible purchase of various assets of the Company." Also, as aside another party who is interested in effecting a reverse merger with the Company has contacted Mr. Silvia, a transaction which, if structured correctly, could lead to additional value for TSCC shareholders.

The only real uncertainty is related to the total estimated liabilities. I must admit that estimating the total amount of such expenses is totally beyond my level of competence. However, I believe a reasonable margin of safety is to increase the high estimate by 10-15%. Under such an assumption total estimated liabilities would range between $2,756,122.6 and $2,881,400.9. Thus, if the non-cash assets are sold for the average of the low and high estimate, or approximately $687,500, then the "likely" distribution could range between $2.36-$2.41/share, which is near the Company's low estimate. The 10-15% increase in high expenses, however, may be entirely unreasonable given that most of the estimated expenses are fixed. Therefore, if we simply use the Company's high estimate as a proxy for total expenses, then the "likely" estimated distribution is approximately $2.51/share, which represents a decent premium to my acquistion price of $2.12/share (approximately 18.39%, or 24.52% on an annualized basis if we assume distriubtions are made on or before December 31st, 2009).

Thursday, March 12, 2009

Roche/Genentech Merger

Today, Roche announced that it would acquire Genetech for $95/share in cash or $46.8 billion Genentech currently trades for $94. I will provide more details after I review the definitive merger agreement and other supplementary materials.

Gilead Sciences/CV Therepeutics Merger

Today, Gilead Sciences (TICKER: GILD) announced that it would acquire CV Therapeutics (TICKER: CVTX) for $20/share in cash or $1.4 billion. I will keep everyone updated on the transaction after I read the definitive merger agreement and other related proxy material. Currently, CVTX trades at a premium to the merger consideration, reflecting the Street's anticipation of another bidder or perhaps a bidding ware between GILD and Astellas tender offer at $16, which the CVTX Board recently rejected.

Return of the Net/Nets

Recent dislocations in US equity markets have caused a resurgence in the number of so called "net/nets." A "net/net" is simply a security whose market value is less than its net current asset value (NCAV), where net current asset value is defined as total current assets less total liabilities (i.e. both short-term and long-term). The term was coined by Benjamin Graham, Warren Buffett's mentor and teacher, who developed a very impressive investment record investing in such securities. The basic investment strategy was to purchase a diversified basket (perhaps 50 or more) of stocks trading at 2/3rds their NCAV and holding them until for about 3-5 years, or until they reached NCAV. The strategy generated annualized returns of approximately 20% per annum during the 20 or 30 some odd years in which Graham implemented the strategy. Unforunately, many of these "net/nets" dissapeared over the years, but now they are beginning to resuface. I conducted a recent scan and was able to identify over 700 securites trading well below their NCAV. Here are a few securities that appared on that list:

1. Tech Data Corporation (TICKER: TECD)

2. Arctic Cat (TICKER: ACAT)

3. Movado (TICKER: MOV)

4. Signet Jeweleres (TICKER: SIG)

5. Electro Scientific Industries (TICKER: EIO)

6. Natuzzi SpA (TICKER: NTZ)

I will begin to manually go through the list of 700 securities to weed out "defective" companies, and will report on any interesting securities that I find.

1. Tech Data Corporation (TICKER: TECD)

2. Arctic Cat (TICKER: ACAT)

3. Movado (TICKER: MOV)

4. Signet Jeweleres (TICKER: SIG)

5. Electro Scientific Industries (TICKER: EIO)

6. Natuzzi SpA (TICKER: NTZ)

I will begin to manually go through the list of 700 securities to weed out "defective" companies, and will report on any interesting securities that I find.

Emageon/AMICAS Tender Offer

My recent risk arbitrage in the Tender Offer of AMICAS for Emageon at $1.82/share seems to be rolling smoothly. The tender commenced as planned on March 5th, my shares have already been tendered, and the spread on the transaction has closed to $0.01 (the stock current trades at $1.81), which suggests the Streets overall confidence in the transaction. I have heard some discussion of potential deal problems related to the Escrow paymenet received from HSS, especially if HSS falls into bankruptcy. I need to look into these problems a little more closely.

Technology Solutions Company Liquidation

On February 10th 2009, the Board of Technology Solutions Company (TICKER: TSCC) approved a Plan of Complete Liquidation and Dissolution of the business, subject to shareholder approval at a yet to be determined special meeting of the shareholders. According to the plan of liquidation, the Company will make an initial liquidating distribution of $2/share in cash upon shareholder approval. The initial liquidating distribution will be distributed from outstanding balances of the firms investment account held at the Harris Bank in Chicago. Moreover, the company plans to monetize its remaining of non-cash assets (primarily accounts receivable and outsanding notes from the sale of certain business subsidiaries), and to the extent possible make additional liquidating distributions to the shareholders. According to Section 3(f) of the plan, the Company estimates that the net realizable value of its assets available for distrubution net of applicable liquidating expenses is approximately $6,350,000, or approximately $2.47/share. The Company's stock currently trades for $2.12. Therefore, a fairly attractive risk arbitrage opportunity seems to be available in the Company's stock. In the best case scenario, you can buy the Company's stock for $2.12, and receive an initial liquidating distribution of $2.00/share, followed by an additional liquidating distribution of $0.47 in, say, a year, a situation yielding an annualized return of approximately 16.5%. In the worse case scenario, you buy the Company's stock for $2.12, receive the initial liquidating distriubution of $2.00/share, but do not receive any additional proceeds from the monetization of its non-cash assets, thereby effectively limiting your downside to approximately 5.6%.

Wednesday, March 11, 2009

Image Entertainment/Q Black Media Merger Update

While there is no question in my mind that both parties want the transaction to close as soon as reasonably practicable, recent payment disruptions with Nyx have made it increasingly obvious that Q-Black Media lacks the financial wherewithal to consummate the transaction. Some have speculated that Q Black Media was exposed to Bernie Madoff, a situation which wiped out the financial resources backing the $100 million Equity Committent Letter. While this is certainly possible, a more reasonable explanation is simply that Q Black Media can't get the equity investors to committ. Irrespective, it is painfully obvious that Q Black is running into financing troubles. The market is currently pricing in over a 70% chance of failure; and given that shareholders have already voted in favor of the transaction, this fact essentially translates into a 70% chance that Nyx doesn't receive the money. Personally, I think the discount is overly pessimistic, especially since no one has any real information related to the financing. In fact, the only guidance we have is that a) Nyx has been stuggling to make the deposis and b) that they are committed to completing the transaction by March 20th. In my opinion, an unbiased estimate should be closer to 50%. While I consider this transaction especially risky there seems to be a good chance for profit should the transaction go through. If Nyx is able to obtain the necessary financing by March 20th, 2009, Nyx will pay $2.75/share in cash. The current per share trading price is $1.38, or approximately 50% discount from the cash consideration value. This translates into a 100% HPR return, or approximately 4800% annualized return (transaction could close in a week). If Nyx is unable to obtain the financing, Image will likely fall to $1 per share, which represent a 27% HPR loss, or approximately 1300% annualized loss. It will be interesting to see what happens.

Arbitrageur

Arbitrageur

Subscribe to:

Posts (Atom)